The National Pension Scheme (NPS) calculator is a convenient online tool that helps individuals estimate the pension amount they can expect upon retirement.

Please follow the steps below to use this NPS calculator –

- Enter Your Monthly Investment: If you plan to invest ₹5,000 every month into your NPS account, type 5000 in the first field.

- Input your expected annual return rate (%): Think of this as the average return you expect per year from your NPS investments. If unsure, you can use a typical estimate like 10.

- Enter your current age (between 18 and 60): This helps calculate the number of years left until retirement at age 60. Just put in your age — like 30, if you’re 30 years old.

- Click the “Calculate” button: The calculator will instantly compute your total corpus at retirement and the mandatory annuity portion (40%), and show a visual breakdown of your investment vs returns.

About National Pension Scheme

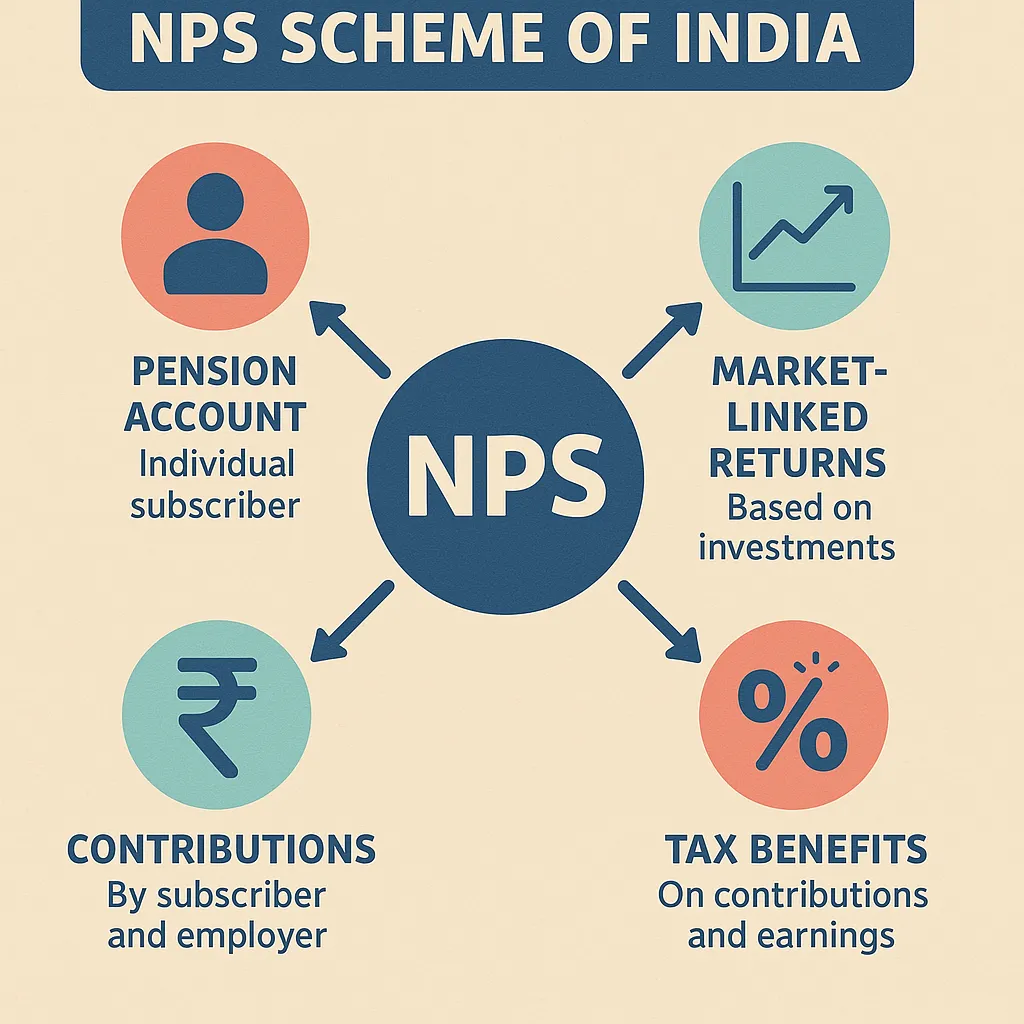

The National Pension System (NPS) is a government-sponsored retirement savings scheme in India, designed to provide financial security and stable income to individuals post-retirement. It is regulated by the Pension Fund Regulatory and Development Authority (PFRDA).

Key Features of NPS:

- Voluntary: Open to all Indian citizens aged between 18 and 70 years.

- Flexible: Individuals can choose their own investment options and pension fund managers.

- Portable: The account remains active across jobs and locations within India.

- Tax Benefits:

- Contributions up to ₹1.5 lakh per annum qualify for tax deduction under Section 80C.

- An additional ₹50,000 can be claimed under Section 80CCD(1B).

- Low Cost: NPS is one of the lowest-cost investment options in India.

Types of NPS Accounts:

- Tier-I Account (Pension Account):

- Mandatory for NPS subscribers.

- Withdrawals are restricted; primarily meant for retirement savings.

- Partial withdrawal allowed under specific conditions.

- Tier-II Account (Investment Account):

- Optional and flexible.

- Allows unlimited withdrawals.

- No tax benefits under 80C.

How It Works:

- Subscribers contribute regularly to their NPS account.

- Funds are invested in various asset classes (Equity, Corporate Bonds, Government Securities).

- On retirement (at 60), up to 60% of the corpus can be withdrawn lump sum (tax-free), and the remaining 40% is used to purchase an annuity for regular pension.

Who Should Invest in NPS?

- Salaried individuals seeking long-term retirement planning.

- Self-employed professionals wanting structured retirement income.

- Anyone looking for a tax-efficient, regulated investment option.